John Key, the former prime minister of New Zealand last week spoke at Ray White’s Connect 2022 conference. One of his current roles is as chairman of the ANZ Bank in New Zealand. Right now, interest rates are rising rapidly in New Zealand and this is having a flow on impact to house prices. After hitting a peak of $1.3 million in November, Auckland’s median has dropped 11 per cent and appears to still be declining. Yet despite this, John Key acknowledged that mortgagee sales remain incredibly rare with the ANZ Bank in New Zealand having just 14 properties on their books.

In Australia, with interest rates increasing, the cost of living rising and particularly high debt levels, there has been a lot of discussion around mortgage stress. The ultimate outcome of mortgage stress is being unable to pay a loan and the property becoming a mortgagee sale.

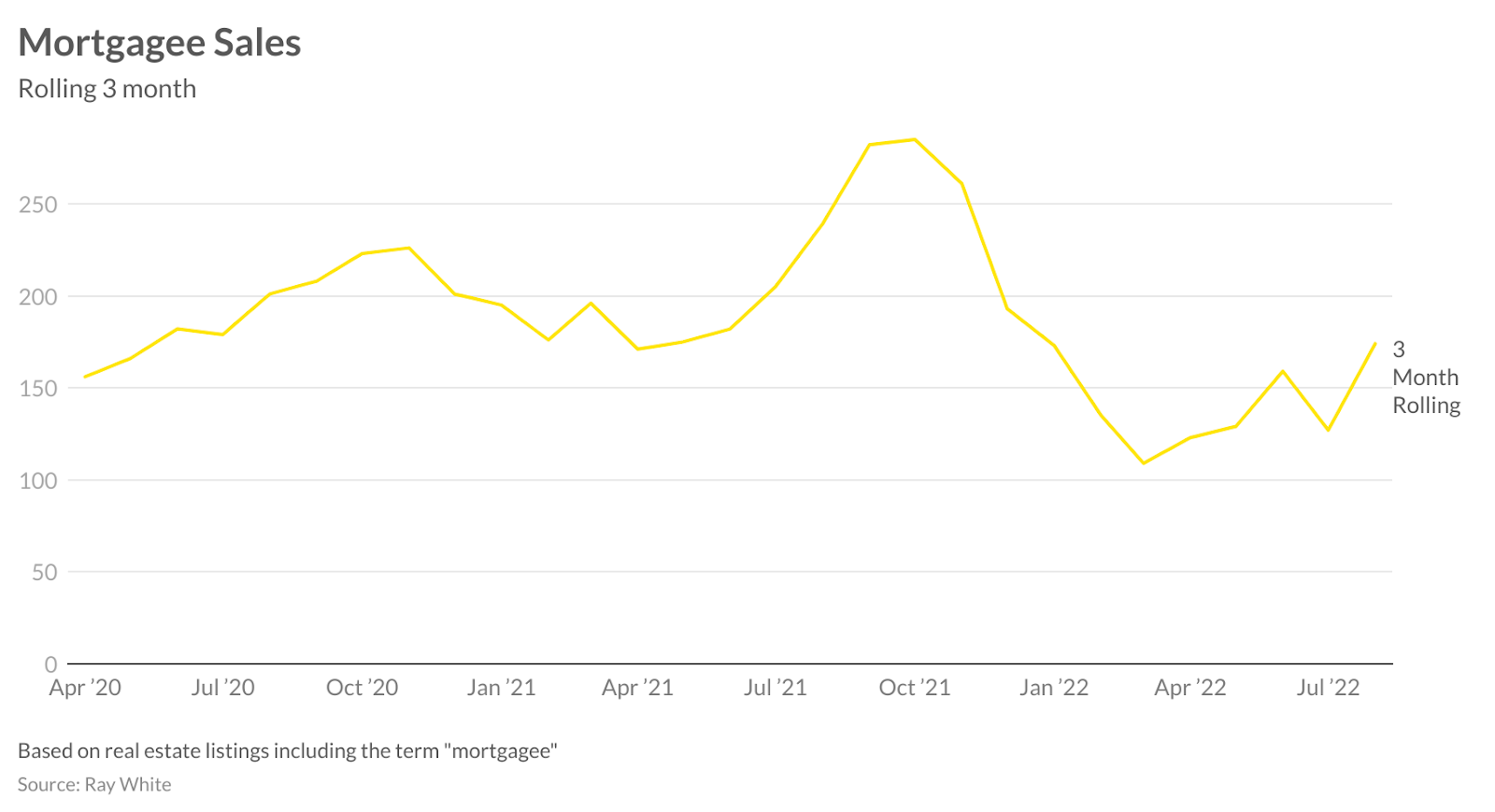

To work out whether there is a rise in mortgagee sales, we looked at real estate listings on Domain and realestate.com.au to see how many homes included the word “mortgagee” back to the start of 2020. From March 2020, there was a gradual increase in the number of mortgagee sales, driven by Australia going into recession during this time. The number of mortgagee sales however didn’t increase as much as they could have during this time given that banks offered six month mortgage payment freezes from the end of March 2020.

By the end of 2020 and early 2021, the number began to fall as property market conditions improved and it became apparent that the short recession was over. Not surprisingly, the biggest increase we saw over this time period was when mortgage payment freezes came to an end in March 2021. Despite a red hot property market, and an economy that was getting back to normal, the number was elevated because borrowers who were in mortgage stress were helped through by the freeze on payments.

Right now, we have seen a pick up in mortgagee sales however at this point they remain below what we have seen through the pandemic. It also highlights how important the support of banks is when it comes to helping people through mortgage stress. There are a number of things that will help people through this period of increasing interest rates. The first is that unemployment is very low, the second is that banks are well capitalised and the third is that savings rates hit record highs during the pandemic.

Finally, the peak of interest rates may be coming sooner rather than later. Bond markets are pricing in Australian interest rates peaking at three per cent early next year, down from 4.5 per cent tipped less than two months ago. Supply chains are now unblocking and fuel prices are coming back. These interest rate rises and the challenges it creates for household balance sheets may be over sooner than we think.

Operating out of Bli Bli’s River Markets, Ray White Bli Bli has long been a cornerstone of the local real estate landscape. Now, an exciting new era begins as Cameron Hackenberg and his wife, Saraya, officially purchase a share in the thriving family business, Ray White Bli Bli. The transition marks a proud milestone for … […]

Nerida Conisbee Ray White Chief Economist Australia’s housing market is now in a coordinated acceleration phase, with every single major market now exhibiting monthly growth rates that signal significant momentum building across the nation. Perth’s 1.3 per cent monthly growth, if sustained, would deliver annual returns well above its current 11.6 per cent annual rate. … […]